* The recent decline in headline inflation is encouraging, but it remains fragile and exposed to external shocks

* Oil price volatility has underscored the structural challenges facing the economy, reinforcing the need for cautious and disciplined monetary policy

* For now, the Reserve Bank of Malawi (RBM) is expected to stay the course, prioritising stability over speed in its policy response

By Chifi Mhango, Chief Economist-Don Consultancy Group

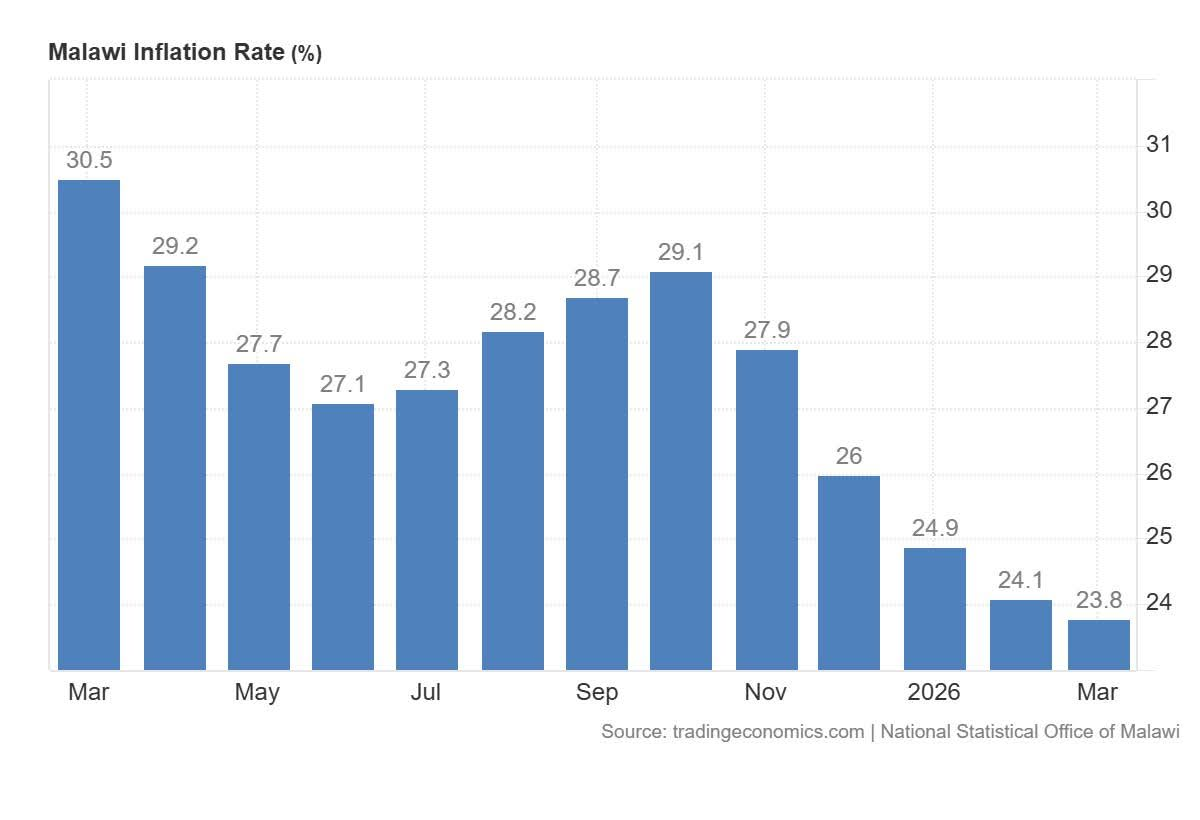

Malawi’s headline inflation is showing a clear, albeit gradual, easing trend, declining from a peak of 30.5% in March 2025 to 23.8% by March 2026, according to the latest data depicted in the figure above.

Advertisement

This downward trajectory signals improving price stability, but the path has not been linear, reflecting the economy’s continued exposure to external shocks, particularly global oil price volatility.

The inflation profile over the past year reveals three distinct phases. The initial period, from March 2025 to June 2025, was characterised by a steady decline in inflation, largely driven by easing food prices and favourable base effects.

This phase provided early signs that inflationary pressures, which had been heavily food-driven, were beginning to subside. However, this progress was interrupted, as inflation began to edge higher again, peaking at around 29.1% in October.

This reversal coincided with renewed pressures from global oil markets. Higher fuel import costs filtered through into domestic prices, raising transportation and production costs across the economy.

In a country like Malawi, where import dependence is significant and foreign exchange constraints persist, such external shocks tend to transmit quickly and broadly into the inflation basket.

Encouragingly, the final quarter of the period into early 2026 shows a more decisive disinflation trend. Inflation declined from 27.9% in November to reaching 23.8% by March 2026, suggesting that earlier shocks are gradually dissipating and that tighter monetary conditions are beginning to anchor inflation expectations.

Improved agricultural output has also played a critical role in stabilising food prices, which remain a key component of the inflation basket.

Nevertheless, the structure of inflation in Malawi is evolving. While food inflation has moderated, non-food inflation, driven by fuel, transport, and utilities, remains persistently elevated.

This shift indicates that inflation is increasingly being shaped by cost-push factors, particularly imported inflation, rather than purely domestic supply constraints.

This dynamic presents a complex challenge for the Reserve Bank of Malawi (RBM). On one hand, the downward trend in headline inflation creates room for policy easing. On the other, the persistence of external risks, especially oil price volatility and exchange rate pressures, necessitates caution.

The policy rate, currently at 24%, is therefore likely to remain on hold in the near term. The central bank is expected to adopt a wait-and-see approach, allowing the disinflation trend to consolidate while monitoring global energy markets and foreign exchange developments.

A premature easing could risk reigniting inflationary pressures, particularly if oil prices spike again or the currency weakens.

Looking ahead, a gradual easing cycle remains plausible, but only under clear conditions. Should inflation continue its descent toward the sub-22% range, the RBM may consider measured rate cuts, potentially in the range of 100 to 200 basis points over the medium term.

However, this will depend heavily on the stability of external conditions and the continued moderation of non-food inflation.

In practical terms, this means that commercial lending rates are likely to remain elevated for longer, reflecting both tight monetary policy and underlying risk premia in the economy. As such, while inflation is moving in the right direction, the broader financial conditions will remain restrictive in the near term.

In conclusion, Malawi’s inflation story is one of progress tempered by vulnerability. The recent decline in headline inflation is encouraging, but it remains fragile and exposed to external shocks.

Oil price volatility has underscored the structural challenges facing the economy, reinforcing the need for cautious and disciplined monetary policy. For now, the RBM is expected to stay the course, prioritizing stability over speed in its policy response.

Chifipa Mhango

* Chifipa Mhango is the Chief Economist and Executive Director of Economic Research & Strategy at Don Consultancy Group, specialising in macroeconomic analysis, public policy, and governance across emerging markets, particularly in Africa. He is known for providing data-driven insights on economic trends, fiscal policy, and institutional accountability, with a strong focus on strengthening economic and governance frameworks.

Advertisement