The Reserve Bank of Malawi

* Malawi doesn’t need exotic tools — it needs credible commitment, a working foreign exchange market, disciplined liquidity, and fiscal backup

* Get those four right, and inflation falls, reserves rise, and the policy rate can safely decline — unlocking investment and jobs

By Duncan Mlanjira

As the nation awaits the final declaration of the September 16 presidential election, Chief Economist for Don Consultancy Group (DCG) outlines a 11-point plan which the next administration should task on the Reserve Bank of Malawi (RBM) as its monetary policy framework — setting a 12 months deadline period.

Advertisement

In a statement, Chifipa, who is DCG’s director of economic research & strategy, indicated that the 12-month playbook for Malawi’s next administration could restore monetary stability and aims at “rebuilding foreign exchange buffers, and lower inflation — anchored in today’s Malawi economic realities”.

He highlights key challenges facing Malawi on the monetary policy front, which include inflation rate still around 27%; policy rate 26%; lapsed International Monetary Fund (IMF) programme; and forex exchange market system misaligned.

Chifipa Mhango has been offering directions on the economic recovery for the past five years

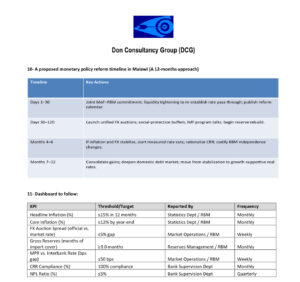

1. Reset the macro anchor (first 30–60 days)

Chifipa proposes that the next government administration should:

* Publicly reaffirm disinflation as priority number one with a target path to bring inflation from ~28% to ≤15% within 12 months and into single digits thereafter. (Signal continuity with RBM’s inflation-targeting framework.);

* Rebuild credibility of the policy rate (26%) by tightening liquidity conditions to ensure effective transmission (fine-tune Open Market Operations, maintain positive real rates until core inflation clearly falls);

* One message, one voice: Launch a joint Ministry of Finance–RBM statement committing to: (i) no monetary financing; (ii) a clear fiscal consolidation path; (iii) transparent foreign exchange market reform. This responds directly to IMF findings on fiscal slippage and foreign exchange distortions.

2. Fix the foreign exchange regime — transparently (days 30–120)

* Move to a single, market-clearing foreign exchange rate using regular, price-discovery auctions (daily/bi-weekly) with full publication of cleared amounts and prices. This addresses the ‘problematic foreign exchange system’ flagged by the IMF and the misalignment concerns in local reporting.

* Unify official, bank, and bureau rates and unwind ad-hoc administrative allocations; replace with a foreign exchange auction and priority window (fuel, fertilizers, medicines) for a limited transition period with donor-backed financing.

* Accumulate reserves opportunistically at auction when the kwacha stabilizes—sterilized to avoid reigniting inflation. Publish monthly reserve and foreign exchange operations dashboards on RBM’s website.

3. Make the interest-rate signal bite (continuous)

* Tight money until expectations break lower: maintain a real positive Monetary Policy Rate while CPI is greater than 20% — avoid premature cuts.

* The trigger to ease should be three tests:

(i) 3-month moving average of core CPI in a clear downtrend;

(ii) foreign exchange auction spreads narrow/stable;

(iii) inflation expectations surveys improve.

* Right-size reserve requirements/Cash Reserve Ratio (CRR) after liquidity normalizes to reduce intermediation costs while preserving control; avoid frequent CRR changes that destabilise bank planning. (RBM used CRR moves this year — use sparingly going forward.)

* CRR is the percentage of a commercial bank’s deposits that the central bank requires banks to keep in reserve (either with the central bank or as vault cash). These reserves cannot be used for lending or investment.

4. Close the fiscal-dominance loop (quarter 1–2)

* Hard budget constraint: Legally cap central-bank credit to government at a low, time-bound ceiling; publish a path to zero direct advances. (fiscal pressures is a key obstacle for Malawi)

* Cash-management reform: Coordinate T-bill issuance calendars with RBM OMOs to smooth liquidity and reduce crowding-out of the private sector.

* Debt operations: Pursue comprehensive debt reprofiling/restructuring to lower rollover risk and interest costs — pre-condition for anchoring inflation expectations.

5. Re-engage the IMF & partners (by month 3)

* Negotiate a new IMF program with upfront structural benchmarks on foreign exchange market unification, fiscal transparency, and RBM independence. The prior ECF expired without a review; a fresh arrangement can catalyse concessional inflows and anchor expectations.

* Front-load social protection (cash transfers) financed by partners to cushion the poor from near-term price effects of foreign exchange normalization—critical for policy durability.

6. Strengthen RBM independence & plumbing (months 1–6)

* Update the RBM Act/regulations to protect the mandate (price stability), prohibit quasi-fiscal ops, and require regular publication of MPC minutes, forecasts, and foreign exchange operations. (Transparency is part of restoring credibility.)

* Modernise monetary operations: Standardise auction-based OMOs, adopt a clear corridor system (standing facilities) around the MPR, and improve payments/RTGS reliability to sharpen transmission.

* Real-Time Gross Settlement (RTGS) is a payment system operated by the central bank that allows banks and financial institutions to transfer money or securities instantly and individually (not in batches).

7. Macro-prudential guardrails (continuous)

* Tighten foreign exchange exposure limits and stress test banks under large-move scenarios during the FX transition.

* Tackle NPLs with time-bound restructuring frameworks and better collateral enforcement; keep capital buffers high until inflation falls decisively. (High inflation + foreign exchange moves can mask asset-quality risk).

Advertisement

8. Communication that anchors expectations (immediately)

* “We will not cut the policy rate until inflation is in a clear, sustained decline and the FX market is functioning normally. As these conditions are met, we will reduce rates gradually.”

* Publish fan charts & scenario paths (oil shock, drought, import-price surge) with the policy response under each scenario so households and firms can plan.

9. Metrics to track (and report monthly/quarterly)

* Inflation: headline & core; target path to ≤15% in 12 months.

* Forex: auction volumes, bid-ask spreads, official vs bureau gap (should converge).

* Reserves: months of import cover (rise steadily).

* Transmission: interbank rates vs. MPR; T-bill yields vs. OMOs.

* Credibility: inflation expectations (surveys/markets) and IMF program milestones.

Chifipa concluded by saying: “Malawi doesn’t need exotic tools — it needs credible commitment, a working foreign exchange market, disciplined liquidity, and fiscal backup.

“Get those four right, and inflation falls, reserves rise, and the policy rate can safely decline — unlocking investment and jobs.

Advertisement